Don't fence me in

ECTA has today published a position paper (beware, it's very short), insinuating that incumbent telcos might use Next Generation Networks as a cynical tool to circumvent regulation and stifle competition. Tisk, tisk. When have we ever seen a regulator ringfence new technology and ignore issues of significant market power? I'm curious to see how much heart the industry can take from the mooted upcoming OFCOM consultation on 21CN.

Tuesday, May 31, 2005

Budget Skype phone

A Diamond Circle mega-value reader writes in with a link to the zero-cost Skype cordless phone, which I'm guessing won't be making an appearance in the Skype shop.

A Diamond Circle mega-value reader writes in with a link to the zero-cost Skype cordless phone, which I'm guessing won't be making an appearance in the Skype shop.

My zero is better than your zero

A couple more examples of EuroTelco pricing itself into oblivion, yesterday from KPN, which has copped the EasyMobile online SIM approach in Germany, and introduced flat rate pricing which is right at the bottom of the current market range, and last Friday from Belgacom, which is seeking to counter the aggression of BASE, Scarlet and others with a flat-rate national calling plan (lots of free minutes, but the EUR0.30 for peak time calls may alienate some users when they realize that their average call duration may be three minutes). Despite the carefree product branding, it is definitely not a "happy time" in EuroTelcoland.

A couple more examples of EuroTelco pricing itself into oblivion, yesterday from KPN, which has copped the EasyMobile online SIM approach in Germany, and introduced flat rate pricing which is right at the bottom of the current market range, and last Friday from Belgacom, which is seeking to counter the aggression of BASE, Scarlet and others with a flat-rate national calling plan (lots of free minutes, but the EUR0.30 for peak time calls may alienate some users when they realize that their average call duration may be three minutes). Despite the carefree product branding, it is definitely not a "happy time" in EuroTelcoland.

Slowing Skype momentum

Readers may have noted that from time to time I report on traffic observations for Skype. I collect these at regular intervals (ideally every day, but sometimes only when I can remember to do so). The last four I have taken (23rd, 26th, 27th and 31st May) all show Skype MoU per day below 40m (vs. an average of 42m in March and April), and the most recent observation showed downloads just above 305k per day (vs. an average of 479k in March and April).

Readers may have noted that from time to time I report on traffic observations for Skype. I collect these at regular intervals (ideally every day, but sometimes only when I can remember to do so). The last four I have taken (23rd, 26th, 27th and 31st May) all show Skype MoU per day below 40m (vs. an average of 42m in March and April), and the most recent observation showed downloads just above 305k per day (vs. an average of 479k in March and April).

Friday, May 27, 2005

Push the button

Readers of this humble bloglet will know that one of my recurring themes recently is the potential for DSL/VoIP/Triple Play markets in Europe to deteriorate into some Three Stooges-like fight, to a soundtrack of M&A advisors' cash registers ringing. I have put together a list of 11 public consolidation candidates, which seems to demonstrate that the market is on message. Average total return in euros over one month for these stocks is 8.3% (10.3% excluding Easynet), vs. 3.8% for the STOXX, and 2.4% for the STOXX Telecom component. In the current climate, I'd be very surprised if these stocks, as a group, don't outperform next month as well. I guess ideally the list should also include Cable & Wireless, due to its relative strength in UK unbundling, but the buyer would have to be in a position to either absorb all the other assets, or break the company up.

11 consolidation candidates and one month performance (EUR)

Easynet Group (UK) : -11.7%

Freenet (Germany) : 17.2%

Fastweb (Italy) : 3.2%

Iliad (France) : 17.8%

Nextgentel (Norway) : 14.3%

Pipex (UK) : 4.4%

Saunalahti (Finland) : 28%

Tiscali (Italy, Netherlands, UK, Germany) : 4.6%

Versatel (Netherlands) : 9.1%

United Internet (Germany) : 1.5%

Web.de (Germany) : 3.1%

Readers of this humble bloglet will know that one of my recurring themes recently is the potential for DSL/VoIP/Triple Play markets in Europe to deteriorate into some Three Stooges-like fight, to a soundtrack of M&A advisors' cash registers ringing. I have put together a list of 11 public consolidation candidates, which seems to demonstrate that the market is on message. Average total return in euros over one month for these stocks is 8.3% (10.3% excluding Easynet), vs. 3.8% for the STOXX, and 2.4% for the STOXX Telecom component. In the current climate, I'd be very surprised if these stocks, as a group, don't outperform next month as well. I guess ideally the list should also include Cable & Wireless, due to its relative strength in UK unbundling, but the buyer would have to be in a position to either absorb all the other assets, or break the company up.

11 consolidation candidates and one month performance (EUR)

Easynet Group (UK) : -11.7%

Freenet (Germany) : 17.2%

Fastweb (Italy) : 3.2%

Iliad (France) : 17.8%

Nextgentel (Norway) : 14.3%

Pipex (UK) : 4.4%

Saunalahti (Finland) : 28%

Tiscali (Italy, Netherlands, UK, Germany) : 4.6%

Versatel (Netherlands) : 9.1%

United Internet (Germany) : 1.5%

Web.de (Germany) : 3.1%

Rocking the cradle

When I was a kid visiting my grandparents in their state-of-the-art 1970s home in Texas, I always thought it was cool that they had a built-in intercom system connecting a number of rooms, though they never seemed to use it. These days they could do it with WiFi and Skype, as a mega-value reader writes in to say:

When I was a kid visiting my grandparents in their state-of-the-art 1970s home in Texas, I always thought it was cool that they had a built-in intercom system connecting a number of rooms, though they never seemed to use it. These days they could do it with WiFi and Skype, as a mega-value reader writes in to say:

"I introduced a friend to Skype. He and his neighbours have younger children. Within 2 weeks all have stared using Skype, have introduced wifi in their homes. Why? Put the laptop (if necessary with an external microphone) or PC with microphone near the baby or children, add a ticking clock as auditive check if the line is open, and voila….

- you can ask neighbours to listen in as a babysit

- you can go to friends, and listen yourself too by using the conference call facility

They love it…"

Thursday, May 26, 2005

Supersize my compliance costs

A multi-platinum value reader writes in to pose an uncomfortable question which has also been stirring in my mind: where does Skype stand in terms of the EU's proposed data retention directive? The consultation document from last year closes with an explicit reference to VoIP, and the latest version of the draft is here. Whether on-net Skype calls would qualify, or conversely fall into some sort of IM limbo, is a question I can't answer - call my lawyer. However, I think other voice service providers would probably argue that if Skype has an inbound and outbound PSTN service, it should be subject to the same compliance regime as they are.

We know from the published traffic stats, user breakdown by country, and the existence of authentication servers that Skype clients obviously can report various forms of information back to the Mother Ship, but consider the costs and operational distractions of compliance with a minimum 12-month retention regime for 1.4m SkypeOut users, or worse, 39m registered Skype users. Where does mega-chat fit in with this? I honestly don't know how valid my concerns are at this point, but given the EU's tendency to crack walnuts with sledgehammers, I'm a bit worried about this one.

Regulatory lawyers out there - as you guys are likely to be among the only industry to make money off of the race to zero, perhaps you could give me a bit of pro bono time on this issue?

A multi-platinum value reader writes in to pose an uncomfortable question which has also been stirring in my mind: where does Skype stand in terms of the EU's proposed data retention directive? The consultation document from last year closes with an explicit reference to VoIP, and the latest version of the draft is here. Whether on-net Skype calls would qualify, or conversely fall into some sort of IM limbo, is a question I can't answer - call my lawyer. However, I think other voice service providers would probably argue that if Skype has an inbound and outbound PSTN service, it should be subject to the same compliance regime as they are.

We know from the published traffic stats, user breakdown by country, and the existence of authentication servers that Skype clients obviously can report various forms of information back to the Mother Ship, but consider the costs and operational distractions of compliance with a minimum 12-month retention regime for 1.4m SkypeOut users, or worse, 39m registered Skype users. Where does mega-chat fit in with this? I honestly don't know how valid my concerns are at this point, but given the EU's tendency to crack walnuts with sledgehammers, I'm a bit worried about this one.

Regulatory lawyers out there - as you guys are likely to be among the only industry to make money off of the race to zero, perhaps you could give me a bit of pro bono time on this issue?

Maltese VoIP

Our friends over at T-REGS point to an interesting study from the Maltese regulator on consumer attitudes and perceptions of the fixed line market. There's some interesting data on mobile substitution, and the revelation that, among those aware of VoIP, it accounts for more than one-third of international calling. It's also telling that nearly two-thirds of this group use more than one provider. Most exciting is the finding that more than half consider VoIP as suitable for primary line replacement.

Our friends over at T-REGS point to an interesting study from the Maltese regulator on consumer attitudes and perceptions of the fixed line market. There's some interesting data on mobile substitution, and the revelation that, among those aware of VoIP, it accounts for more than one-third of international calling. It's also telling that nearly two-thirds of this group use more than one provider. Most exciting is the finding that more than half consider VoIP as suitable for primary line replacement.

Crack pipe

Still sifting through lots of email, I find that a mega-Platinum value reader late last week called my attention to consultations on MSOs with significant power in the Dutch market (found here, for Dutch speakers or quick learners). Effectively, the Dutch regulator has extended the 18 EU market definitions to include broadcast as a 19th market, and kicked off a process for potentially imposing cost controls. This development is strangely absent from UGC's website... My reader's take on the consultations follow (his words):

Conclusions:

Still sifting through lots of email, I find that a mega-Platinum value reader late last week called my attention to consultations on MSOs with significant power in the Dutch market (found here, for Dutch speakers or quick learners). Effectively, the Dutch regulator has extended the 18 EU market definitions to include broadcast as a 19th market, and kicked off a process for potentially imposing cost controls. This development is strangely absent from UGC's website... My reader's take on the consultations follow (his words):

Conclusions:

- All Dutch MSO's effectively have no competitors in their territories (nor has the consumer a real choice)

- The 'big five' (UPC, Casema, Essent, Multikabel and Delta) together hold 93% of all subs

- Small MSO's charge between euro 7 and euro 10 for a basic package ofsome 30 TV - the large MSO's charge from 14 to almost euro 16 (UPC) for the same

- OPTA suspects that the 'big five' MSO's on the wholesale market make use of their monopoly to refuse entrance for competitors - and on both wholesale and retail markets to charge excessive rates, discriminate in price & quality, use delaying tactics and cross subsidize.

Intended measures:

- OPTA differentiates between the small, not-for-profit utility-like MSO's and the big five- the small ones will have to explain to their subs how their tariffs are built up (some do this already)

- The big ones will have to open their administrations to OPTA, so that the regulator can decide what tariffs will be acceptable

- When excessive tarifs are discovered, the MSO's in question will be ordered to lower their prices.

An earlier decision by OPTA (June 2004) has some predictive value. They then decided, based on accountant reseach of Multikabel's bookkeeping, that at realistic network costs and a realistic ROI, Multikabel could charge euro 0.11 per 8 mhz video channel to Canal+ (so: 30 channels is euro 3,30, plus charges for content including advantages of scale would end up in an UPC rate of some euro 7 - effectively 50% of today's rate)

In the next 4 months the MVO's can send in their comments, in September the accountant research can start, leading to final decisions in mid 2006.

Near-freedom of speech

Telenor has (kind of) responded to Tele2's recent pricing salvo. Free 3G video calling for six months and EUR0.10 MMS handsets.

Open the door

One of the issues I touched on in Stockholm was the emerging need to start looking beyond the "voice market" as such, and focus on how VoIP becomes more integrated as a feature of everyday life. Here's one inspiration (though expensive and not VoIP), and another interesting example of the success of commonsense applications.

One of the issues I touched on in Stockholm was the emerging need to start looking beyond the "voice market" as such, and focus on how VoIP becomes more integrated as a feature of everyday life. Here's one inspiration (though expensive and not VoIP), and another interesting example of the success of commonsense applications.

Pedal to the metal (copper)

Cable & Wireless, reporting full year results to 31st March today, reveals that its Bulldog broadband unit has reached its 400 exchanges target seven months ahead of schedule, and is now to accelerate its unbundling rollout, adding 200 more this year, and again in 2006/07. The company is also launching a new SoHo product in June, including up to eight VoIP lines.

UPDATE: Do we sense that somehow BT is growing more concerned about the threat from full unbundling, or is this announcement pure coincidence?

Cable & Wireless, reporting full year results to 31st March today, reveals that its Bulldog broadband unit has reached its 400 exchanges target seven months ahead of schedule, and is now to accelerate its unbundling rollout, adding 200 more this year, and again in 2006/07. The company is also launching a new SoHo product in June, including up to eight VoIP lines.

UPDATE: Do we sense that somehow BT is growing more concerned about the threat from full unbundling, or is this announcement pure coincidence?

Wednesday, May 25, 2005

A little knowledge is a dangerous thing

I always appreciate a bit of exposure, but I have to say that I have some big problems with this post at Business Week, citing me as an apparent vindication for a view that telecom is poised for some sort of reinvention, in a positive sense. Firstly, I disagree strongly with the assertion that Europe is somehow structurally incapable of promoting innovation. Institutionally, and at a macroeconomic level, yes, large parts of Europe may be screwed, but if we're talking telecom, then let's acknowledge that both Skype and SIP are European in origin, and as I hopefully demonstrated in Stockholm yesterday, I think we can reasonably state that European countries are at the forefront of VoIP adoption (as has also been shown to be the case with P2P).

Whatever his underlying case for arguing that Europe and Japan lack "killer apps" (a very curious oversimplification of some very complex market dynamics), where the author really misses the clue train is in the fact that the really important developments unfolding now are ultimately about a huge technology revolution driven by consumer empowerment, or, as Espen Fjogstad from Telio states, "a genuine unbundling of the last mile in a way which regulation has failed to deliver." In other words, it's a partial transfer of market value/wealth, in which some disappears (or reverts to the consumer), and some moves to non-traditional beneficiaries. However, I believe the overall effect will be profoundly deflationary in the aggregate.

My statement that EuroTelcoland was awakening to the threats facing it was not underpinned by any serious optimism. Admitting to the threat is rational, but the reactions to it may not be. So far, the flurry of M&A activity (which has been repeatedly documented here ad nauseum) fills me with unpleasant flashbacks to the Quixotic mobile land-grab of the 1997 - 2000 period, albeit with lower absolute cash outlays. Nevertheless, I would argue that the business case assumptions may be no more sound.

Historically, there seemed to be an unwritten rule that, regardless of what happened in mobile, the PTTs would never mess around with one another's traditional voice markets, but the gloves are now off. I fear that the incumbents are now well on the way to destabilizing both their voice and DSL markets to a crisis level, driven by what they believe to be the priorities of the capital markets. Again, let's think back to the 3G auction period and recall just how disastrously the markets misread that situation. Moreover, based on the investors I speak to, I can't find any consensus which would support such a strategy - rather, I think the market will increasingly react with alarm at the looming IP nuclear arms race.

That said, I have never argued that outright EuroTelcocide was likely, but rather that the incumbents of the future will have to be dramatically smaller and learn to live with far less, and that this process of transformation will be an excruciatingly difficult one. Culturally, I sense that many of them are still too wrapped up in notions of their own significance and growth potential to accept the cold reality of an insurrection jointly mounted by consumer choice, generational change, technological innovation/subversion, the agendas of global internet/media gorillas, and outright bloody-minded troublemakers from leftfield like Skype (long may they run).

Despite the dramatic recovery in balance sheets since meltdown in 2000, EuroTelcos collectively still have debts well in excess of a large number of national GDPs (take any three of the large cap stocks and you soon get to a number well over EUR100bn), as well as pension liabilities, an issue on which the airline industry offers little comfort. As I've undoubtedly said before, the next few years are going to be a fascinating and horrifying spectacle in EuroTelcotown, as innovation cycles compress and the incumbents struggle to adapt to a dynamic for which they are inherently ill-suited.

Yes, Mr. Dude, telecom is undergoing a revolution, but revolutions are intended to depose those in power, and revolutions frequently kill lots of people and give rise to all sorts of other dislocations which few could have foreseen earlier. Revolutions never result in the former ruling class having a higher standard of living as a result. One thing I notice from my Sitemeter tag is that the traffic driven to the site from this article is a lot lower than one would expect from a publication like Business Week. Maybe telco is not the only industry in the midst of a revolution.

I always appreciate a bit of exposure, but I have to say that I have some big problems with this post at Business Week, citing me as an apparent vindication for a view that telecom is poised for some sort of reinvention, in a positive sense. Firstly, I disagree strongly with the assertion that Europe is somehow structurally incapable of promoting innovation. Institutionally, and at a macroeconomic level, yes, large parts of Europe may be screwed, but if we're talking telecom, then let's acknowledge that both Skype and SIP are European in origin, and as I hopefully demonstrated in Stockholm yesterday, I think we can reasonably state that European countries are at the forefront of VoIP adoption (as has also been shown to be the case with P2P).

Whatever his underlying case for arguing that Europe and Japan lack "killer apps" (a very curious oversimplification of some very complex market dynamics), where the author really misses the clue train is in the fact that the really important developments unfolding now are ultimately about a huge technology revolution driven by consumer empowerment, or, as Espen Fjogstad from Telio states, "a genuine unbundling of the last mile in a way which regulation has failed to deliver." In other words, it's a partial transfer of market value/wealth, in which some disappears (or reverts to the consumer), and some moves to non-traditional beneficiaries. However, I believe the overall effect will be profoundly deflationary in the aggregate.

My statement that EuroTelcoland was awakening to the threats facing it was not underpinned by any serious optimism. Admitting to the threat is rational, but the reactions to it may not be. So far, the flurry of M&A activity (which has been repeatedly documented here ad nauseum) fills me with unpleasant flashbacks to the Quixotic mobile land-grab of the 1997 - 2000 period, albeit with lower absolute cash outlays. Nevertheless, I would argue that the business case assumptions may be no more sound.

Historically, there seemed to be an unwritten rule that, regardless of what happened in mobile, the PTTs would never mess around with one another's traditional voice markets, but the gloves are now off. I fear that the incumbents are now well on the way to destabilizing both their voice and DSL markets to a crisis level, driven by what they believe to be the priorities of the capital markets. Again, let's think back to the 3G auction period and recall just how disastrously the markets misread that situation. Moreover, based on the investors I speak to, I can't find any consensus which would support such a strategy - rather, I think the market will increasingly react with alarm at the looming IP nuclear arms race.

That said, I have never argued that outright EuroTelcocide was likely, but rather that the incumbents of the future will have to be dramatically smaller and learn to live with far less, and that this process of transformation will be an excruciatingly difficult one. Culturally, I sense that many of them are still too wrapped up in notions of their own significance and growth potential to accept the cold reality of an insurrection jointly mounted by consumer choice, generational change, technological innovation/subversion, the agendas of global internet/media gorillas, and outright bloody-minded troublemakers from leftfield like Skype (long may they run).

Despite the dramatic recovery in balance sheets since meltdown in 2000, EuroTelcos collectively still have debts well in excess of a large number of national GDPs (take any three of the large cap stocks and you soon get to a number well over EUR100bn), as well as pension liabilities, an issue on which the airline industry offers little comfort. As I've undoubtedly said before, the next few years are going to be a fascinating and horrifying spectacle in EuroTelcotown, as innovation cycles compress and the incumbents struggle to adapt to a dynamic for which they are inherently ill-suited.

Yes, Mr. Dude, telecom is undergoing a revolution, but revolutions are intended to depose those in power, and revolutions frequently kill lots of people and give rise to all sorts of other dislocations which few could have foreseen earlier. Revolutions never result in the former ruling class having a higher standard of living as a result. One thing I notice from my Sitemeter tag is that the traffic driven to the site from this article is a lot lower than one would expect from a publication like Business Week. Maybe telco is not the only industry in the midst of a revolution.

`Why the waffle?

Apologies for the obvious Belgian stereotyping. I'm still trying to catch up on blog-reading, and just noticed an interesting post in which JC highlights moves by KPN's Belgian mobile subsidiary BASE to attack incumbent Belgacom's fixed line business (and it's not just the fixed - the Proximus mobile unit today cut revenue and EBITDA guidance). I particularly like the senior citizen discount angle. At a purely propagandistic level, I'm amazed that there is no mention of this in KPN's corportate website. It's your own subsidiary, it's doing something interesting in a market where analysts have been skeptical of your prospects, and you apparently don't want to get any mileage from it. Curious.

UPDATE: Looking through my mountain of unopened email, I realize that another super-value reader sent me this story late last week, and I missed it. Apologies. It also seems that rumors are afoot that BASE may be developing a DSL strategy for the Belgian market. Another chapter in mutual annihilation begins.

Apologies for the obvious Belgian stereotyping. I'm still trying to catch up on blog-reading, and just noticed an interesting post in which JC highlights moves by KPN's Belgian mobile subsidiary BASE to attack incumbent Belgacom's fixed line business (and it's not just the fixed - the Proximus mobile unit today cut revenue and EBITDA guidance). I particularly like the senior citizen discount angle. At a purely propagandistic level, I'm amazed that there is no mention of this in KPN's corportate website. It's your own subsidiary, it's doing something interesting in a market where analysts have been skeptical of your prospects, and you apparently don't want to get any mileage from it. Curious.

UPDATE: Looking through my mountain of unopened email, I realize that another super-value reader sent me this story late last week, and I missed it. Apologies. It also seems that rumors are afoot that BASE may be developing a DSL strategy for the Belgian market. Another chapter in mutual annihilation begins.

Superminiaturize my triple play

I've said in the past that the harder the entertainment world works to persecute file sharers, the more serious the response would become. Azureas and the original BitTorrent are gradually moving towards a distributed model, and a web crawling Torrent search engine is in the works. With metered voice going the way of the Dodo, and EuroTelcos using DSL to poke each other in the eye, my prediction is that this time next year we will be seeing industry conferences focusing on "The Telco Single Play."

I've said in the past that the harder the entertainment world works to persecute file sharers, the more serious the response would become. Azureas and the original BitTorrent are gradually moving towards a distributed model, and a web crawling Torrent search engine is in the works. With metered voice going the way of the Dodo, and EuroTelcos using DSL to poke each other in the eye, my prediction is that this time next year we will be seeing industry conferences focusing on "The Telco Single Play."

Hijack the web to promote the deflationary spiral

A Diamond Club mega-value reader calls my attention to some of the amazing things being done with the Greasemonkey extension to the Firefox browser, which allows annotation to websites. The guys over at Overstimulate are doing some interesting things to deliver open source comparison shopping in the online book and travel industries, and I wonder what guerilla marketing opportunities we may see develop around this. (Someone else has been working on an extension for browser based BitTorrent, but the trail seems to have gone cold.)

A Diamond Club mega-value reader calls my attention to some of the amazing things being done with the Greasemonkey extension to the Firefox browser, which allows annotation to websites. The guys over at Overstimulate are doing some interesting things to deliver open source comparison shopping in the online book and travel industries, and I wonder what guerilla marketing opportunities we may see develop around this. (Someone else has been working on an extension for browser based BitTorrent, but the trail seems to have gone cold.)

Skype loves Paris in the springtime

Reuters newswire is reporting (in French, which I read only very poorly) that Niklas Zennstrom, speaking at a Reuters event today in Paris, has confirmed that Skype expects to be cash flow positive in 2005, and also that the company currently has 2.2m users in France, which is 1m more than the last update I had last month. Sacre blu!

Reuters newswire is reporting (in French, which I read only very poorly) that Niklas Zennstrom, speaking at a Reuters event today in Paris, has confirmed that Skype expects to be cash flow positive in 2005, and also that the company currently has 2.2m users in France, which is 1m more than the last update I had last month. Sacre blu!

VON impressions, et al

Other commitments brought me back to London after my presentation at VON, so here's a summary post about yesterday in Stockholm and a bit of related newsflow.

VON

Other commitments brought me back to London after my presentation at VON, so here's a summary post about yesterday in Stockholm and a bit of related newsflow.

VON

- Turnout looked very strong to me. I'd guess there were about 400 people in the main sessions in the morning, peaking with Niklas Zennstrom's SRO presentation (Jeff later informed me that the room held 600, and there was an overflow room next door with a video feed from the main room).

- Presentations were, as to be expected, a bit of a mixed bag, though most touched on common themes of transparency, ease of use, and the essential need to understand consumer thinking and needs.

- It seems like some presenters believe they need to chart the history and future evolutionary paths of a variety of technologies in order to have a discussion, which takes up a lot of time and leads to needless repetition. Personally, I'm tired of looking at network layer diagrams.

- Jeff Pulver and Niklas both, as usual, touched on a number of interesting issues, familiar to readers of this bloglet or those who have seen them present elsewhere.

- Both spent a considerable amount of time on regulation issues. I have been concerned for some time that Skype has a rapidly increasing risk profile in terms of regulatory creep, and this issue is now being taken up vigorously by Om and Martin. I'm not sure how convinced the audience was by the "if a burglar were in my house I'd want to IM the police, not call them" argument employed by Niklas, but he obviously has to fight his corner.

- My presentation was the usual mix of cheerleading and predictions of imminent doom.

- Part one was an overview of where we are today, and why the industry (such as it is) can feel justifiably proud of its achievements. "VoIP" returns more hits on Google than Elvis Presley, Paris Hilton or Our Lord, and Skype is bigger than the Beatles. Combined access-related VoIP subscribers, access independent subs and Skype users in France and Germany leads to a raw penetration rate of around 30% of the addressable markets in those countries (not adjusting for any double-counting). In Europe there is a direct correlation between broadband penetration and Skype user numbers, with countries like Sweden, Switzerland, and Denmark boasting Skype user numbers which seem to equate to 25 - 30% of broadband users. Five of the top ten Skype user countries are in Europe, which is interesting in light of the fact that Europe accounts for less than a third of global broadband user numbers. Norway may be VoIP's single biggest success story to date, with Telio subscribers accounting for more than 1% of the population of the country, and 7% of broadband connections. Putting Vonage US on the same penetration level would give it about 3.5m subs. Lesson - innovation from the edge works and there's room for everyone to compete.

- That was the Woodstock interpretation. The Altamont version of the story is that incumbent complacency has ended, and the PTTs seem to be speaking more frankly and raising their game. From my perspective, this quarter there was a palpable sense of crisis which has not been so present before. This spells danger, particularly as the EuroTelcos seem to regard IP as the new catalyst to drive M&A activity, and a buzzword to wow the capital markets. I gave the examples which have been repeatedly documented in this blog. I also spent some time discussing the fact that I wouldn't expect the IM incumbents to roll over and die, as Yahoo! recently demonstrated with its newlook client. I later met a member of the audience from MSN, a nice guy whose business card identified him as a key player in "Voice Services." (Only last week I got to rub shoulders with another nice guy from AOL UK, who left me with the distinct impression that EuroTelcos may underestimate this company at their peril, a point I have made previously.) Suffice it to say that, as far as I can see, the IM platforms in Europe generate similar levels of daily usage to that of Skype, but they are much larger user bases, and also part of a broader strategy. It would be naive to assume that they are not sharpening their knives for something more aggressive. I also discussed brand extenders like Man U and Chelsea, which ostensibly have radically different agendas in the broadband world. After this downbeat assessment, I closed with some challenges/opportunities, in terms of more granular and intelligent presence, closer integration with consumer activities (customer websites, online gambling, online gaming, the ego-casting arena, etc.) and devices. All familiar stuff to anyone who has read this blog previously (or one of the many sources which inspire me).

- Other observations - I seemed to see a lot more incumbents present than I have previously, and I also had the sense that this was part of a stepped-up effort to assess the real issues in the market (back to my earlier point on complacency rapidly being a thing of the past). I was also amazed to see that there were no sell-side analysts there, at all. It increasingly occurs to me that there is potentially a viable research model involving strictly industry events such as this one, because the chances to meet key people in operational roles are numerous, and there is a lot of interesting industry intelligence flying around at all times. It's a huge chance to learn, but maybe Stockholm was too remote, or maybe the people in question are just too damned clever.

Related newsflow - I'm trying to catch up with a number of stories related to VoIP, so here goes, in no particular order:

- Cablecom, reporting Q1 results today, has seen 24% sequential growth in VoIP subs over Q4's level. Penetration of the broadband base now stands at 44%, up from 38% in Q4 and 29% in Q3. Interestingly, sequential growth in broadband connections was stronger this quarter than in Q4 - perhaps there is some synergistic effect from VoIP.

- KPN launched a bundled VoIP/DSL product today, initially on a limited basis. Pricing looks a little half-hearted to me. I also see that 100 new DSL subs stand to win an Xbox, copy of Halo2 and a year's subscription to Xbox Live! (now there's a real VoIP service!).

- As I hinted briefly in a post last week, SIPfoundry yesterday unveiled their open source attack on proprietary PBXs, Microsoft LCS and Skype. Interesting to note here that fully one-third of the developer community is European.

- As also hinted at in some recent posts, Popular Telephony yesterday unveiled its particular take on co-opting the Skype network and community, a version of PeerioBiz with Skype gateway.

- Our friends at Paradial in Norway, which I have written about from time to time, yesterday unveilved further enhancements to the already impressive RealTunnel, including multiparty conferencing also open to external SIP clients/servers.

- Skype launched an affiliate program, bringing Skype superdistribution to the masses as a paying proposition (I will keep my dayjob, for now).

- Global Crossing launched European inbound and outbound services yesterday, which seems to yet again lower the barriers to entry for access-independent players in the European markets.

- I also had a chance to catch up with Kerry Ritz, MD of Vonage UK. Try as I may, I couldn't get any subscriber numbers out of him, though he described himself as very satisfied with what they've done so far. At least one very happy Vonage UK customer was stood nearby (who happened to be a BT employee.)

Monday, May 23, 2005

Stockholm calling

In case anyone thought this was all glamor, here's the view from my hotel in Stockholm - shot with a Microsoft smartphone, moved to my laptop via USB cable, uploaded to Flickr via my inclusive hotel WiFi connection, and published via Blogger - telco revenue = 0.

Anyway, I think this VON may hold some interesting announcements, not least of all from Popular Telephony. Both Martin and Richard have recently made some compelling posts on Skype stickiness and the underlying value of the Skype community as a distribution network (not a million miles away from my own long-standing suspicion that Skype's true value lies in P2P super-distribution). Popular Telephony will tomorrow announce a development which is yet another angle on this theme.

Invading your consciousness

A Telenor ad on the long row of plasma screens playing a loop of commercials on the express train platform at Stockholm Arlanda Airport.

Supersize my apathy, 2

My office in my pocket? That sounds painful, not to mention highly intrusive.

Supersize my apathy

I had a little time to kill today at Heathrow Terminal 1, which, like the rest of BAA's portfolio of torture-chambers-posing-as-airports, is actually a gigantic shopping mall where planes happen to take off and land. Just one minute walk from the T-Mobile hotspot (tended by, not one, but two, attractive young women in magenta skirts, who swore up and down that several people a day pay up for access) was the gigantic Vodafone sales and display area. Lots of David Beckham and flashy video clips, but no one looking to buy, as far as I could see. The largest number of people I saw anywhere near the stand was a group of elderly Japanese tourists who were using it as a gathering point.

Nordic IP explosion

I'm about to leave for VON in Stockholm, but a couple of newsflashes are in order:

I'm about to leave for VON in Stockholm, but a couple of newsflashes are in order:

- In a further extension of the "IP as blunt weapon of EuroTelco mutual annihilation" theme, Telenor has today announced acquisitions in both of its neighboring markets. Telenor is paying SEK6bn, or 3x 2004 sales, for Bredbandsbolaget, Sweden's number two broadband services company, with 335k subs (80k of whom are VoIP users), and also taking out Cybercity, number three in Denmark. Total consideration, including assumed debt, works out at around NOK6.5bn, or EUR800m to acquire 425k customers. Punchy.

- Over the weekend, I received word that Telio's 2004 results showed positive net income, and an EBITDA margin of 12.2% on turnover of NOK42.8m in 2004. Apparently the company is to report earnings quarterly from now on.

UPDATE @ 18:31 CET: Coincidentally (;-0), shares in Nextgentel closed up 6.4% today...

Thursday, May 19, 2005

It cuts both ways

I don't know if this sort of issue is prevalent or newsworthy in countries outside the UK, obsessed as it is with the youth lawlessness, but I would be interested to receive word of any examples from elsewhere in Europe. Interestingly, today we get news of the lowly mobile phone, not as agent of outrage and cheap, malicious thrills, but rather as the protector of civil liberties. Now there's some serious disruption.

I don't know if this sort of issue is prevalent or newsworthy in countries outside the UK, obsessed as it is with the youth lawlessness, but I would be interested to receive word of any examples from elsewhere in Europe. Interestingly, today we get news of the lowly mobile phone, not as agent of outrage and cheap, malicious thrills, but rather as the protector of civil liberties. Now there's some serious disruption.

Letter from America

It's rare that a friend asks for advice and I feel unequivocally confident in my response, but today was a happy exception. I genuinely received the following email today from an old friend who is an independent web designer and film maker in the American heartland:

"Dear Jimbob,

Is there any way to post a movie using BitTorrent and get paid by people who download it? My new project has been languishing, but I am starting to shoot again and I'm hoping to get a BFD kind of audience (instead of the smallish reception our earlier documentary encountered). Obviously I do not live in Hollywood so I must plan for an alternate distribution method in the event that no one in the mainstream wants to distribute it. I also like the idea of it being on the outside."

A few weeks ago I might have scratched my head inconclusively over this one, but now I can answer in one word, which is a good feeling. The word is Prodigem. My friend, wandering blindfolded in the world of distribution, can now go and pin the long tail on the donkey.

It's rare that a friend asks for advice and I feel unequivocally confident in my response, but today was a happy exception. I genuinely received the following email today from an old friend who is an independent web designer and film maker in the American heartland:

"Dear Jimbob,

Is there any way to post a movie using BitTorrent and get paid by people who download it? My new project has been languishing, but I am starting to shoot again and I'm hoping to get a BFD kind of audience (instead of the smallish reception our earlier documentary encountered). Obviously I do not live in Hollywood so I must plan for an alternate distribution method in the event that no one in the mainstream wants to distribute it. I also like the idea of it being on the outside."

A few weeks ago I might have scratched my head inconclusively over this one, but now I can answer in one word, which is a good feeling. The word is Prodigem. My friend, wandering blindfolded in the world of distribution, can now go and pin the long tail on the donkey.

Ripple effect

Via a double platinum value reader, more evidence that it won't be long before we see Skype in use on a prime time drama series. BBC television's Money Programme is going to air a feature on VoIP and Skype tomorrow evening. The article quotes BT's head of Wholesale predicting the death of telephony, as such, within 10 years, and also offers a testimonial from an 82 year-old Skype granny. There's your tipping point.

Via a double platinum value reader, more evidence that it won't be long before we see Skype in use on a prime time drama series. BBC television's Money Programme is going to air a feature on VoIP and Skype tomorrow evening. The article quotes BT's head of Wholesale predicting the death of telephony, as such, within 10 years, and also offers a testimonial from an 82 year-old Skype granny. There's your tipping point.

Wednesday, May 18, 2005

W(h)ither, IP Triple Play?

Today I chaired the first day of the Osney Media IPTV & Telco Triple Play Forum in London. What distinguishes the Osney events from others I have attended is that the organizers seat participants in small roundtable groups, careful to separate company/industry cliques, and are intent on throwing difficult questions and issues out to these "nodes" to digest and regurgitate back to the audience/presenters. This provides some immediate feedback to the presenters and stimulates various strands of discussion which are absent in the standard "one-to-many followed by questions from the floor" formula.

As someone who is a confirmed pessimist about EuroTelcoland's long term prospects, I found it refreshing, because the 60 or so people in attendance (mostly high-level strategy, business development and innovation people, about half of whom were from incumbents) seemed surprisingly open and willing to accept that they are in a very tenuous position, and that expectations are very low.

This echoes some of the franker messages coming from some management teams in this quarter in investor briefings, but also highlights the absurdity of broker absence from these sorts of events, in favor of other, higher profile industry hype events, or indeed their own "industry conference" propagandoramas. I was the only broker there today, and there were no buy-side people, and only one consultant. Everyone else was from the operating lines in industry (service provision/infrastructure/security) - not the kind of people we in the sell-side world (at least at my level) normally have access to - and the ones I met were open and straight-up in a way that we normally don't hear from top management or their IR avatars. Unsurprisingly, I came away from the event feeling like I got a greater sense of where these people/companies were emotionally, and that is a very, very difficult place. I felt impressed with the industry's growing willingness to challenge itself and to question its own assumptions about the recipe for long-term survival, though ultimately I was no more convinced that there is much which telcos can do about it.

Though the audience repeatedly expressed doubts as to whether the industry was smugly assuming that it knew what consumers want, this group appeared to be one of the better-informed to which I have spoken over the past two years. I normally like to start off these kinds of events by taking a straw poll of the audience on a number of issues, which has previously yielded some fairly appalling results, though today's group shaped up like this:

Broadband users - 90%

Household WiFi users - 80%

Skype users - 50% (why do the telcos continue to play down the Skype threat, when their own employees are repeatedly exposed as avid fans?!)

BitTorrent users - 5%

EDonkey users - 2%

Those who feel they understand what BitTorrent/EDonkey are - 20%

Those who feel they understand what KaZaA is - 40%

Online photo storage/sharing users - 2%

Blog readers - 5%

iPod owners - 20%

Owners of MP3 players of any description (including iPods) - 50%

Portable video player owners - 3%

PVR owners - 8%

Overall, I think these numbers are not bad, though whether this reflects how rapidly awareness has grown over the past year, or whether it is something to do with the individuals and their corporate roles/mandates, is impossible to answer.

I don't have the time or energy to relate the gist of each presentation, but the summary takeaway points collected from the various roundtables, as reported in the wrap-up session, were:

- It is refreshing to be brought down to earth, and have our assumptions challenged (as moderator, I tried to be moderate, despite my pessimism, but Nigel Walley from Decipher gave the audience a good dose of reality in his presentation, which they seemed to appreciate).

- Partnerships between suppliers/operators/content owners have to move beyond current master/slave relationships if we are all to stand a chance of survival.

- There is no clear path to defining future direction. We have not yet found a key differentiator for the kind of services we are considering. This is an area which the global internet players could end up owning entirely. (I mentioned in passing that a good illustration of this was the forays by Yahoogle [a la "Oxbridge" as a collective noun for Oxford and Cambridge] into local listings and search, a natural advantage the EuroTelcos should have, if only they hadn't sold their directories businesses under financial duress, wrongly believing them to be "old economy.")

- It is difficult to define the balance between IP Triple Play as defensive or opportunistic strategy, but we acknowledge that it is something we probably have to do in any event, even if there is no material contribution to earnings.

- There is a clear tension between corporate demands to deliver results/growth, cost restraints placed upon us in getting there, and the management of expectations in the public arena (both consumer and capital markets).

- Understanding the consumer experience is paramount, and a different corporate mindset is required to get there. (Personally, I think every day about Richard Stastny's recent observation - "You can compete with everyone, but you cannot compete with your customer." Many in the audience seemed to regard as novel, even startling, Nigel Walley's focus on using the consumer point of view as a strategic starting point [I agree with him entirely], which confirms my sense that there are still some bridges to cross in this regard.)

On balance, the presentation which seemed to resonate most with the audience, was the case study presented by Helmut Leopold of Telekom Austria. In it, he detailed the experience of the company in embracing the "long-tail" principle in the town of Engerwitzdorf, which independently produced over 70 videos in its first four months, ranging from dramas to documentary and public affairs content, and now constitutes a dedicated channel on the Telekom Austria TV platform.

The operational uplift for TA was a dramatic increase in local DSL penetration (the locals needed to buy in to the technology to be able to distribute and consume their own content) and the creation of an additional channel on the platform which is unique, yet which required no programming or production costs. I got the sense from listening to him that one prong of the TA TV strategy is to become a facilitator of locally produced, local interest programming, which differentiates the channel offering at limited cost, while driving stickiness on both the access and TV platforms. This struck me as, counterintuitively, both a crafty and proactive move in content creation/aggregation, and a partial capitulation to the "dumb pipe" principle. No wonder, then, that this particular section of the session ended with a number of delegates (overwhelmingly from Eastern/Central Europe, where I guess that local market content may be relatively under-represented in the broadband landscape) surrounding Mr. Leopold to learn more.

Asked what would prevent another player from doing the same, Mr. Leopold replied, "Nothing," but he noted that so far, voice competitors remain focused on killing each other in voice, and the cable content aggregators view the whole issue as too threatening. I found myself struggling to believe that what I was hearing was an incumbent telco actively embracing "decentralized media" principles (albeit for its own selfish ends), rather than focusing exclusively on delivering a me-too TV product based solely on prominent national and global brands. Perhaps the market particulars of Austria have engendered this to a large extent, but it was refreshing and thought-provoking, nevertheless. I asked about the cultural transformation required to get to this point, and issues cited were investment in OSS/BSS, changes in work practices (help desk calls are more intensive on the weekend now, versus weekdays previously), and a more complex customer management environment (troubleshooting is more complicated, which necessitates a lot of training for call center staff).

Overall, this was an interesting day, which afforded much more insight into true telco thinking than the entirety of Q1 conference calls I have listened to so far. Based on what I saw and heard today, it would be wrong to say that the industry (at least as represented by these strategy and business development people) is deluded about its prospects, though how representative across large organizations is the pragmatism I heard today, is something I question. The only disappointment for me (and many others, apparently) was the unexplained absence of BT Retail's head of Entertainment, Andrew Burke. BT apparently wasn't interested in sending a replacement for him, and this led to all sorts of speculation (not helped by the fact that BT is reporting full year results tomorrow).

My sense from today was that, collectively speaking, the EuroTelco beast has genuinely awakened to some significant extent, and is thirsting for new ideas and approaches for digging itself out of some deep caca. IP TV/triple play may be an admittedly half-hearted initial attempt to develop into something else, though I am skeptical as to whether the macro environment really lends itself to any self-help strategies, no matter how clever. Nevertheless, what is different, from what I observed today, is a sort of openness and (dare I say it?) humility, among strategy and bizdev people, to admit what they don't know, and to seek out the darker corners of some complex issues in a bid for some kind of survival.

Tuesday, May 17, 2005

The IPWireless mystery in Europe

I've written a few times about IPWireless, and in my attempt to catch up on blogreading tonight, I came across this piece from Nancy Gohring at WiMax Networking News. I'm dying to know who the operator in question is. I have a hard time imagining that it's Europe's largest cellco, mainly due to its steadfast historical avoidance of any exposure to "fixed" broadband, and also the fact that the company seems to be trying to achieve fixed line displacement through existing 3G properties.

That really only leaves T-Mobile and Orange, among "pretty significant" European players, in the sense of companies which are present in a significant number of markets beyond their home markets. Orange parent France Telecom is going hell-for-leather in DSL in the UK, Netherlands and Spain, which makes the wireless cannibalization risk pretty high. Deutsche Telekom has targeted DSL growth in France and Spain, but is present in neither mobile market. On the contrary, DT's position in mobile in the UK and the Netherlands is unenviable, and it has no DSL position to sacrifice in either market. However, DT is the chief European proponent (and financial backer) of Flarion. All-in-all it's a complicated prospect for these two.

Perhaps the "pretty significant" designation extends to the next tier of players, namely KPN and O2? These companies seem to be less conflicted by DSL/FWA investments (and O2 has a legacy of fixed line service displacement). If anyone has any theories/views/news, I would be very curious to know.

UPDATE: A mega-uber value reader points to this earlier story identifying Orange France as one, but is it the same as what Nancy has heard?

I've written a few times about IPWireless, and in my attempt to catch up on blogreading tonight, I came across this piece from Nancy Gohring at WiMax Networking News. I'm dying to know who the operator in question is. I have a hard time imagining that it's Europe's largest cellco, mainly due to its steadfast historical avoidance of any exposure to "fixed" broadband, and also the fact that the company seems to be trying to achieve fixed line displacement through existing 3G properties.

That really only leaves T-Mobile and Orange, among "pretty significant" European players, in the sense of companies which are present in a significant number of markets beyond their home markets. Orange parent France Telecom is going hell-for-leather in DSL in the UK, Netherlands and Spain, which makes the wireless cannibalization risk pretty high. Deutsche Telekom has targeted DSL growth in France and Spain, but is present in neither mobile market. On the contrary, DT's position in mobile in the UK and the Netherlands is unenviable, and it has no DSL position to sacrifice in either market. However, DT is the chief European proponent (and financial backer) of Flarion. All-in-all it's a complicated prospect for these two.

Perhaps the "pretty significant" designation extends to the next tier of players, namely KPN and O2? These companies seem to be less conflicted by DSL/FWA investments (and O2 has a legacy of fixed line service displacement). If anyone has any theories/views/news, I would be very curious to know.

UPDATE: A mega-uber value reader points to this earlier story identifying Orange France as one, but is it the same as what Nancy has heard?

Fade to black

Mon amis-du-blog JC has some invaluable observations on the shell-shock Belgian cable is feeling in the wake of Belgacom's football rights coup. The MSOs have pushed the McKinsey button after only one week - it must be serious.

Mon amis-du-blog JC has some invaluable observations on the shell-shock Belgian cable is feeling in the wake of Belgacom's football rights coup. The MSOs have pushed the McKinsey button after only one week - it must be serious.

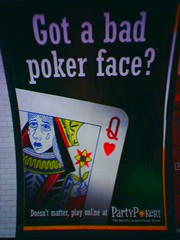

Put up or shut up

Not a great photo, admittedly, but my cameraphone can't deal with the curvature of the Tube. I spent a long time on the London Underground today, and these ads are everywhere, for online gaming site PartyPoker.com. In case you can't make it out, it reads, "Got a bad poker face? Doesn't matter, play online." Message: it's an anonymous, non-social activity.

I've written on this before, but I think this is exactly the wrong message to be sending. Beyond the monetary aspect, the "glamor" of the casino (at least as portrayed in myriad films) is in styling and profiling, and engaging in the drama around the table (even though this seldom seems to be the case in reality). But anyway, we're talking about online gambling and fantasy, so why not feed the delusions of the players, with audio/video, or visual/voice avatars? Why this industry isn't taking note of what's happening in the real online gaming phenomenon is beyond me.

The opposite of hype

One week ahead of VON Europe (I'll be there, as one of few non-Swedes on the bill on the morning of day one) and the inevitable barrage of press releases, I had dinner last night with Dean and TJ from VoipUSER. It was refreshing to hear their view of things, driven, as it is, by a love of the technology and a genuine enthusiasm for spreading the word, rather than a commercial agenda or world domination aspirations. The site is a rallying point for advocates/developers, a point of entry for newcomers, and a testbed for new ideas. In other words, it's not a million miles away from the Skype forums, albeit on a smaller scale, and devoted to open source (incidentally, watch this space).

I am also interested to see how their self-funding community outbound service develops. Users are issued with an 0844 number in the UK, which generates GBP0.03 per minute in revenue, which is then used to purchase outbound minutes for the community to use. As I write this, the community (around 7,000 users) has c.22k minutes on account. The other aspect I think is interesting is the potential to push this service further out into the world. VoIPUSER already peers with FreeWorldDialup and Gossiptel, the latter of which is a charter member of XConnect, which makes me wonder about the scope for peering with other members. One message I have been trying to share with our clients for years now is not to underestimate small players with agendas different from the orthodoxy. This may be another case in point.

One week ahead of VON Europe (I'll be there, as one of few non-Swedes on the bill on the morning of day one) and the inevitable barrage of press releases, I had dinner last night with Dean and TJ from VoipUSER. It was refreshing to hear their view of things, driven, as it is, by a love of the technology and a genuine enthusiasm for spreading the word, rather than a commercial agenda or world domination aspirations. The site is a rallying point for advocates/developers, a point of entry for newcomers, and a testbed for new ideas. In other words, it's not a million miles away from the Skype forums, albeit on a smaller scale, and devoted to open source (incidentally, watch this space).

I am also interested to see how their self-funding community outbound service develops. Users are issued with an 0844 number in the UK, which generates GBP0.03 per minute in revenue, which is then used to purchase outbound minutes for the community to use. As I write this, the community (around 7,000 users) has c.22k minutes on account. The other aspect I think is interesting is the potential to push this service further out into the world. VoIPUSER already peers with FreeWorldDialup and Gossiptel, the latter of which is a charter member of XConnect, which makes me wonder about the scope for peering with other members. One message I have been trying to share with our clients for years now is not to underestimate small players with agendas different from the orthodoxy. This may be another case in point.

Podcasting for the masses

Maybe Radio 4 listeners aren't "the masses" as such, but it's probably fair to say that they represent a wide range of the UK population, and I wouldn't say that much of the Radio 4 programming is skewed towards technophiles to any extent. It's all the more indicative of where we are in media evolution, then, that this morning on the way to work I heard a news segment devoted to the BBC's podcasting trial. Commercial radio may well tremble at the directions Auntie is taking. GCap Media last week reported pro forma advertising revenues down 17% YoY in April, and Chrysalis expects radio revenues to be down 5 - 6% for the full financial year to August. We may argue about how much of this is cyclical, and how much a structural shift, but the BBC is in an enviable position to embrace some disruptive influences, and there are other mechanisms out there to give the consumer greater control of the listening experience. Are we eventually looking at overt product placement in music? If so, these people are visionaries...

Anyway, there's much, much more to come.

Maybe Radio 4 listeners aren't "the masses" as such, but it's probably fair to say that they represent a wide range of the UK population, and I wouldn't say that much of the Radio 4 programming is skewed towards technophiles to any extent. It's all the more indicative of where we are in media evolution, then, that this morning on the way to work I heard a news segment devoted to the BBC's podcasting trial. Commercial radio may well tremble at the directions Auntie is taking. GCap Media last week reported pro forma advertising revenues down 17% YoY in April, and Chrysalis expects radio revenues to be down 5 - 6% for the full financial year to August. We may argue about how much of this is cyclical, and how much a structural shift, but the BBC is in an enviable position to embrace some disruptive influences, and there are other mechanisms out there to give the consumer greater control of the listening experience. Are we eventually looking at overt product placement in music? If so, these people are visionaries...

Anyway, there's much, much more to come.

Post-telco era

The UK Royal Mail, which launched its HomePhone CPS product back in January, today reported that it took on 60k customers (see page 10) in the first 10 weeks of operation. Admittedly, 6,000 net adds per week is fairly anemic relative to TalkTalk's 10,200 during the quarter, but the P.O. is a newcomer and has to overcome some perceptual challenges. Nevertheless, the number is better than I would have expected from a standing start, and if they achieved that sort of growth without putting a dent in Carphone Warehouse's numbers, then I'm even more curious than ever to see BT Group's KPIs on Thursday.

The UK Royal Mail, which launched its HomePhone CPS product back in January, today reported that it took on 60k customers (see page 10) in the first 10 weeks of operation. Admittedly, 6,000 net adds per week is fairly anemic relative to TalkTalk's 10,200 during the quarter, but the P.O. is a newcomer and has to overcome some perceptual challenges. Nevertheless, the number is better than I would have expected from a standing start, and if they achieved that sort of growth without putting a dent in Carphone Warehouse's numbers, then I'm even more curious than ever to see BT Group's KPIs on Thursday.

Monday, May 16, 2005

Do you want to watch?

Back in February I published an excruciatingly long note on BSkyB and the changes occurring within broadcasting which should make investors wary. One of the risk factors I cited was that sports and content rights holders would increasingly choose a more direct route to the end consumer, as has been the case with Major League Baseball. Manchester United has taken step one (note the appeal for expressions of interest from non-UK residents), and speculation is mounting that suitor Malcolm Glazer is going to boost cash flow by opting out of the Premiership's collective rights negotiations process and going it alone (will the floodgates open behind him?). To add insult to injury, the Financial Times reported at the weekend that viewing of Premiership matches on Sky's platform was down 9% YoY in the most recent season. No wonder Sky has sought to play up the importance of cricket recently.

Back in February I published an excruciatingly long note on BSkyB and the changes occurring within broadcasting which should make investors wary. One of the risk factors I cited was that sports and content rights holders would increasingly choose a more direct route to the end consumer, as has been the case with Major League Baseball. Manchester United has taken step one (note the appeal for expressions of interest from non-UK residents), and speculation is mounting that suitor Malcolm Glazer is going to boost cash flow by opting out of the Premiership's collective rights negotiations process and going it alone (will the floodgates open behind him?). To add insult to injury, the Financial Times reported at the weekend that viewing of Premiership matches on Sky's platform was down 9% YoY in the most recent season. No wonder Sky has sought to play up the importance of cricket recently.

More Q1 updates - Spain

Telefonica, reporting today, says it has nearly 33k subs on its Imagenio IP TV platform at the end of April, nearly 1% of the addressable number of households in the footprint. April net adds were nearly equal to the total for all of Q1, and gross adds are running at 3,500 per week, or 0.4% penetration added monthly.

Telefonica, reporting today, says it has nearly 33k subs on its Imagenio IP TV platform at the end of April, nearly 1% of the addressable number of households in the footprint. April net adds were nearly equal to the total for all of Q1, and gross adds are running at 3,500 per week, or 0.4% penetration added monthly.

Skyped out

Skype Journal points to some interesting data suggesting a slowdown in growth rates for Skype, based on the rate of increase in concurrent user numbers. I also track a few stats (daily downloads and daily minutes of use), and I can see a similar trend. Throughout March, average daily downloads were running between 450 - 500k, though in April this fell to the 380 - 430k range, and so far in May we are consistently below 400k (most recent observation over the weekend was just 320k). Admittedly, it's always slower on the weekend, but my stats suggest a 9% decrease over the level of the previous weekend.

The Skype Journal post rightly points out that there have been relatively fewer releases of late, so perhaps that is a contributing factor, but what about the usage side of things? In both March and April, the average of my observations of daily MoU were 41.7m per day. So far in May, we are at 39.9m, despite more concurrent users online and a larger overall user base. Is average Skype usage growing less intensive? Possibly. The weather is improving, even in England. Other possible explanations which spring to mind are:

Skype Journal points to some interesting data suggesting a slowdown in growth rates for Skype, based on the rate of increase in concurrent user numbers. I also track a few stats (daily downloads and daily minutes of use), and I can see a similar trend. Throughout March, average daily downloads were running between 450 - 500k, though in April this fell to the 380 - 430k range, and so far in May we are consistently below 400k (most recent observation over the weekend was just 320k). Admittedly, it's always slower on the weekend, but my stats suggest a 9% decrease over the level of the previous weekend.

The Skype Journal post rightly points out that there have been relatively fewer releases of late, so perhaps that is a contributing factor, but what about the usage side of things? In both March and April, the average of my observations of daily MoU were 41.7m per day. So far in May, we are at 39.9m, despite more concurrent users online and a larger overall user base. Is average Skype usage growing less intensive? Possibly. The weather is improving, even in England. Other possible explanations which spring to mind are:

- Skype's differentiation as an IM client is gaining traction, and this is diluting voice usage. Overall stickiness may be increasing, but this doesn't show up in the MoU stats, which are one dimensional.

- SkypeOut/SkypeIn usage scenarios are increasing their share of overall usage, which again is something invisible in the MoU stats.

Perhaps it's time for Skype to start breaking out other KPIs so we can better understand how usage is evolving. Publishing SkypeOut minutes, SkypeIn minutes, and IM sessions would give a much clearer and well-rounded picture, wherein on-net MoU alone may be less meaningful over time.

Friday, May 13, 2005

UK cable watch

Just trying to catch up on results which I wasn't able to follow in real time this week:

Just trying to catch up on results which I wasn't able to follow in real time this week:

- NTL - Triple play penetration up to 24.6%, digital TV penetration at 70.8%, CATV overall lost subs again, but unlike Q4 last year, digital TV showed net growth.

- Telewest - Triple play penetration 30.3%, total CATV grew and digital CATV was up another 27k (which is nearly one third of what Sky added in a much smaller footprint), and the company is now at 87% digital TV penetration. They have now taken the decision to shut the analogue service down in 2006, and reallocate bandwidth to some supercharged broadband products.

Half way through a lost decade

I remember when a telecom analyst was something to be, a solid career choice. "Doctors and lawyers may come and go, but there'll always be demand for a telecom analyst, my boy," I can recall my dad telling me when I was just a lad. Well, not actually. AT&T was THE telco when I was a lad, and BT's ground-breaking IPO wasn't even a twinkle in Mrs. Thatcher's eye.

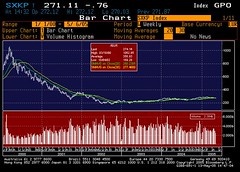

Swisscom's invocation of "millenium hype" yesterday made me think back fondly to those days of 97 - 2000 and predictions of "Cisco as the first $1trn company," and an IPO pipeline of European mobile assets that seemed full to the point of bursting. So, sentimental fool I am, I went and pulled this chart from Bloomberg. As a telco analyst, I'm a quarter of the man I used to be, according to this, and EuroTelco has underperformed its broader STOXX index by 47%. Plus, as I highlighted recently, the current technical indicators are looking poor, and what newsflow we have had to date has been pretty relentlessly uninspiring at best. As the great Sylvia Wadhwa once famously said, "There's just one word for it, and that word is 'ouch'."

More updates from the front

Tiscali reported Q1 yesterday, and from a pan-EuroTelco disruption standpoint, highlights were:

Tiscali reported Q1 yesterday, and from a pan-EuroTelco disruption standpoint, highlights were:

- 1.2m DSL subs in the markets they remain in, of which nearly a fifth are on unbundled lines. Given the still-pathetic state of unbundling in the UK, I assume most of these are concentrated in the Netherlands and Italy.

- The company has added around 135k DSL subs in the UK, which is sequential growth of 36%. Wanadoo, which is nearly half again as large, added 148k in the quarter.

More cracks in the facade

Swisscom's Q1 report yesterday gave us another indication of the state the fixed line sector is in: local and long distance voice traffic was down 11.5% YoY, traffic revenue was down 12% YoY, PSTN line loss was 3%, ISDN is now decisively ex-growth. Management, having for a long time downplayed the impact of Cablecom, admitted that their cable rival is by far their most serious competitor and is now visibily hurting Swisscom on the access side of the business. Management cut the revenue guidance for 2005 by 4%, and shaved EBITDA guidance by 2.4%. Choice quotes from the presentation:

CEO Jens Alder also made a reference to perhaps EUR75bn in cumulative cash flow over the coming years from the European sector after buybacks and dividends - cash which will be looking for a home, and he seemed to be predicting a coming M&A wave. In fact, he cautioned of a return to "millenium hype" acquisition strategies. All this sounds comfortingly familiar, and it's refreshing to hear a company speak so frankly about the challenges facing EuroTelcoland and the dangers inherent in a desperate quest for growth backed by a mounting cash pile and access to cheap debt.

Swisscom's Q1 report yesterday gave us another indication of the state the fixed line sector is in: local and long distance voice traffic was down 11.5% YoY, traffic revenue was down 12% YoY, PSTN line loss was 3%, ISDN is now decisively ex-growth. Management, having for a long time downplayed the impact of Cablecom, admitted that their cable rival is by far their most serious competitor and is now visibily hurting Swisscom on the access side of the business. Management cut the revenue guidance for 2005 by 4%, and shaved EBITDA guidance by 2.4%. Choice quotes from the presentation:

"Organic and non-organic expansion of telco players leading to

increased competition in all markets and segments."

"Customer awareness forcing all players to make offers ever more

compelling and attractive. Customers expect to receive better services at

lower prices."

CEO Jens Alder also made a reference to perhaps EUR75bn in cumulative cash flow over the coming years from the European sector after buybacks and dividends - cash which will be looking for a home, and he seemed to be predicting a coming M&A wave. In fact, he cautioned of a return to "millenium hype" acquisition strategies. All this sounds comfortingly familiar, and it's refreshing to hear a company speak so frankly about the challenges facing EuroTelcoland and the dangers inherent in a desperate quest for growth backed by a mounting cash pile and access to cheap debt.

Skype as MVNO

In a few recent posts I've expressed concerns that, through SkypeOut and SkypeIn, Skype may have exposed itself to a number of regulatory complications at national level in many of the countries where its users live. Andy has found evidence that they are moving to shape the regulatory debate in the US, indicating that the company is indeed sensitive to its exposure.

I particularly like the revelation on page 2 that:

I draw from this that the mobile strategy may go way beyond deals like iMate and Motorola, perhaps encompassing an outright branded MVNO-type service. Preposterous, you say? Skype's head of operations and paid services, named in the document, is ex-Tele2 and a savvy pioneer of the MVNO space.

In a few recent posts I've expressed concerns that, through SkypeOut and SkypeIn, Skype may have exposed itself to a number of regulatory complications at national level in many of the countries where its users live. Andy has found evidence that they are moving to shape the regulatory debate in the US, indicating that the company is indeed sensitive to its exposure.

I particularly like the revelation on page 2 that:

"Indeed, Skype is planning to integrate its IP offerings with its own WiFi

handsets and will support the provision of reliable user location information to

emergency services when consumers buy those handsets."

I draw from this that the mobile strategy may go way beyond deals like iMate and Motorola, perhaps encompassing an outright branded MVNO-type service. Preposterous, you say? Skype's head of operations and paid services, named in the document, is ex-Tele2 and a savvy pioneer of the MVNO space.

Thursday, May 12, 2005

Do you see what I see?

Deutsche Telekom results today - messy, confusing (IFRS restatements, new reporting structure, reclassifications of all sorts of data), and not terribly inspiring. The main area of interest from the point of view of this bloglet is an apparent doubling in the rate of decline in PSTN/ISDN lines (-400k) in the quarter, for an annualized rate of 4.4%. Management were frank in admitting that DSL unbundlers are pressurizing the voice market, as I expected already. Sipgate's 100k, plus maybe 300 - 400k on Freenet/United Internet VoIP products, plus another c.1.4m Skype accounts (and whatever number may be using DT's own VoIP product). Whatever double-counting may be involved here, I think it's safe to say that we're probably looking at a market of at least 2m VoIP users, or nearly 1/3 of the broadband users in the country.

And we're just getting started: hot on the heels of its partnership with debitel, QSC today acquired celox, which expands its footprint to 1000 central offices in 100 German cities. I'm left wondering how long it will be before another PTT decides to move into Germany, either organically, or more likely through acquisition. IP services are the new 3G (albeit with lower barriers to entry and less capex), and DT is in the game, though the game in France may have just gotten a lot tougher. How DT gains 15 - 20% of a market where the top three control 89% is a tough question to answer with hard work alone. Any guesses what 20Mbps in France will cost this time next year?